Turning the Annual SMB Loan Review Process into an All-the-Time Review Process.

In the first blog of this series, we focused on how innovation in SMB lending will help credit unions and community banks acquire and grow small business relationships. Part 2 of this series will focus on the annual loan review process, and how a little innovation can help you to streamline this resource-intensive activity. We also introduce the concept of an all-the-time review process that is more effective for proactively managing SMB loan default risk and growing your loan portfolio through timely customer advice and services.

Knowing your small business loan portfolio

Annual loan reviews are important for any financial institution to monitor how their small business loan portfolio performed over the last year. It is a chance to ensure that the credit risk assessment of small businesses is still accurate and current. The annual loan review process exists to minimize the potential risk of an unexpected loss and identify any business or collateral changes that may have happened since the loan was approved. It also presents a great opportunity to confirm that your small business members are happy and you are meeting their service requirements and expectations.

But is once a year really enough?

Weathering the inefficiencies and shortfalls of an annual review

Although annual loan reviews are considered a critical element for effective portfolio risk, it takes a lot of time and resource effort to prepare the documentation, projections and advice storyline. Small business advisors need to do a deep dive into credit history, cash flow history and projections for the business. They may need to assess collateral available (if dealing with secure loans). Often, they will also need to assemble owner character references and other pieces of supporting loan documentation such as business and personal financial statements, income tax returns and a business plan. This process takes several hours, spread over several days, frequently happening several months after year end.

And still, we ask the question, is once a year really enough?

Another challenge with the annual loan review process is the focus spent looking at past performance data instead of what is happening with small businesses in real-time. When we are dealing with a highly volatile business environment, as seen now and predicted well beyond the COVID-19 pandemic, it becomes quite clear that:

A yearly loan review is really NOT enough.

Unlocking real-time cash flow data and analytics for an all-the-time loan review process

Einstein once said that insanity is doing the same thing over and over again, and expecting different results. Innovation in SMB lending presents a unique opportunity for credit unions and community banks to rethink the annual loan review process, and consider what it would mean to shift loan portfolio management from a backward-looking historical data review process, to keeping a continuous, proactive pulse on small business performance. This is what can be achieved by unlocking, monitoring and analyzing real-time cash flow data.

Innovating your SMB lending so that you can automatically categorize and analyze banking transactions means that customers can constantly share their cash flow data to increase the speed of advice and financing decisions. Time historically spent by SMB lending advisors to gather, process and validate financial statements can more re-focused on supporting more clients with forward looking advice and service offerings that will expand your relationship with small business members. The ability to monitor and analyze cash flow data for every small business loan applicant means you can:

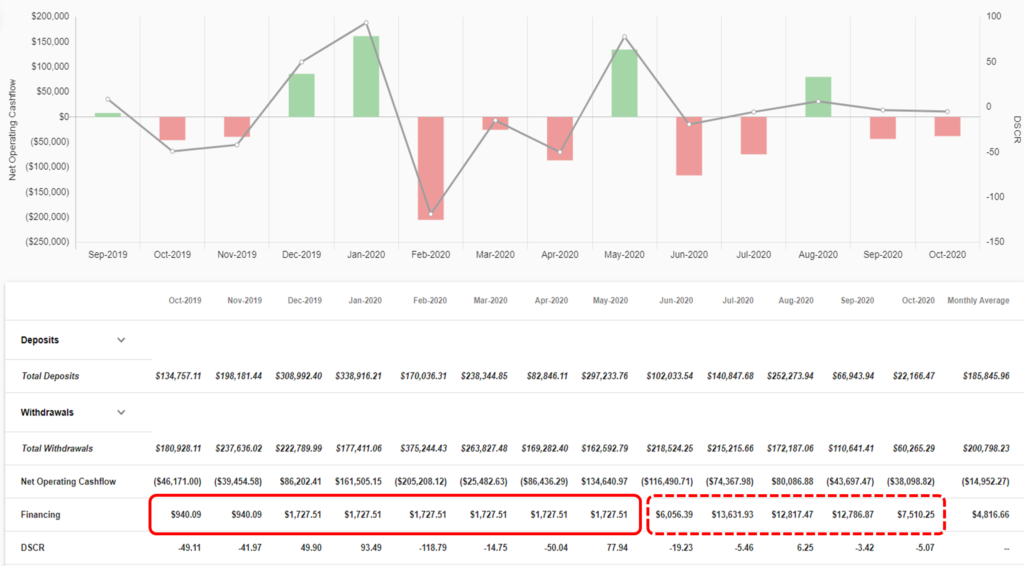

- Review withdrawals, deposits, transfers, recurring payments and other debt/credit payments on a month-by-month basis, to help both the SMB owner and the financial lender understand the current and future, not just historical, status of the business.

- Streamline the manual loan review process by automatically constructing a “synthetic” small business income statement that enables you to review financial status faster (and way more often) than annually.

- Augment traditional credit bureau scores with relevant cash flow data, achieving a 30-50% performance lift over traditional consumer credit scores.

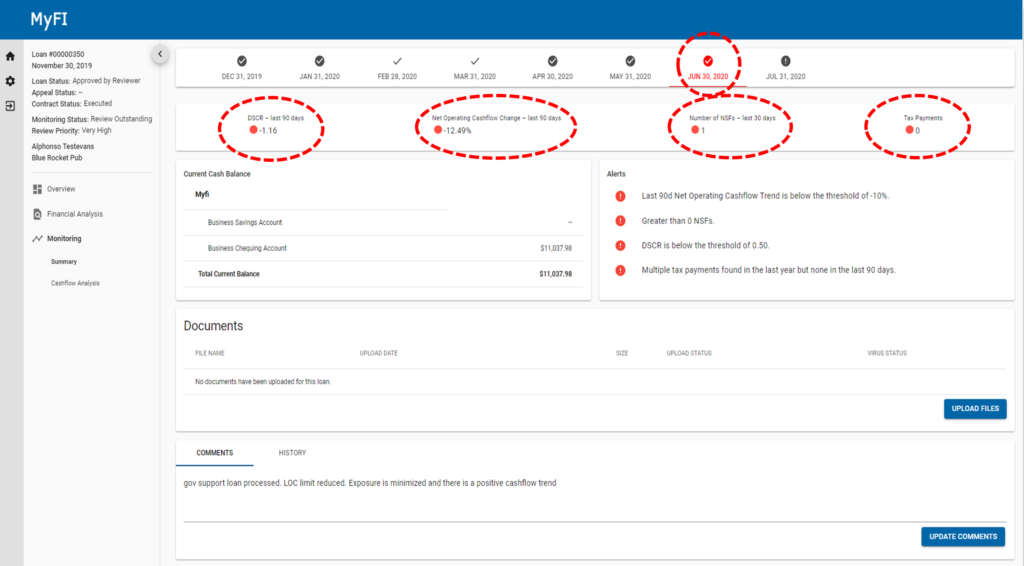

- Continuously monitor financial cashflow metrics and be instantly alerted to predictive success and predictive risk indicators such as the debt service coverage ratio, negative account balance trends, operating debit trends, new line of credit payments or NSF transactions.

- Reduce portfolio risk, while enabling your SMB advisors to proactively offer advice and extend services that help SMBs grow their business – not just annually, but when they need it the most.

Continuous cash flow monitoring: Capture and categorize monthly payment deposits/withdrawals. Analyze financing payments, debt service coverage ratios and net operations cash flow.

Real-time cashflow alerting: Flag anomalies and outliers indicating positive or negative changes in SMB cash flow.

In summary, with a little innovation in your SMB lending, you could streamline the annual loan review process and spend less time and effort constructing a picture of past performance. You can focus on how to better service small businesses now and predict their needs for tomorrow. For a deeper discussion on the benefits of turning the annual loan review process into an all-the-time process, contact us or book a demo.

Take a look at part 3 of this SMB lending series, where we’ll look the benefits of cloud-based SMB lending technology.

Share this article

Related Posts