Acquiring and growing small business relationships.

These next few blogs are meant to help credit unions and community banks build out an undisputable business case for making innovation in small to medium-sized business (SMB) lending a top 2021 priority. We’ll start by exploring what it takes to acquire and grow SMB relationships – and where they go if you don’t.

Just to be clear, taking an effective, scalable approach to your SMB lending does not mean turfing the personal relationships and going “all digital”. In fact, credit unions and community banks will most likely lose less to the big banks and fintech players if you make “localized people who really care” your superpower. Innovation in SMB lending simply means putting the needs of your small business customers, both new and growing, at the center of your SMB lending platform & strategy. With a bit of technology investment and minimal implementation time, you can:

- Build out a faster, less cumbersome loan process

- Unlock more data sources to make obtaining credit easier

- Provide the business insights and advice SMBs need to grow their business

These key advancements will make SMBs excited to engage with your community bank or credit union. Let’s explain how.

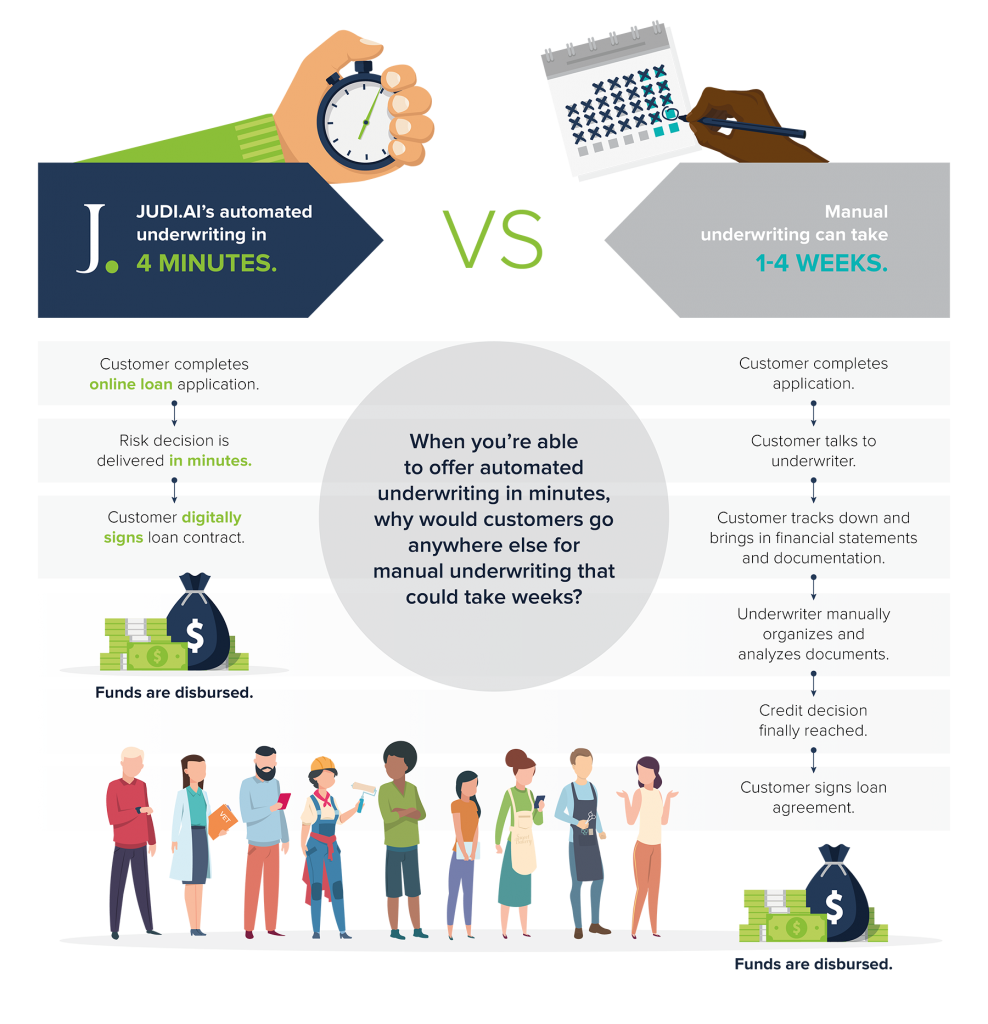

Building out a faster, less cumbersome loan process

When it comes to automating the underwriting process, SMB lending innovation means you can take a manual process that averages a completion time of 1-4 weeks, down to 4 minutes. Not only is that powerful productivity gains for your team, but faster funding means happier customers. They have more time to focus on the success of their business, which is really what they want to do. (As a bonus side benefit, more satisfied SMB customers will also translate into more referrals – who can complain about that?). While these time savings are impressive and a great step towards making SMB lending easier, the innovation advantage does not end there.

Unlocking more data sources to make obtaining credit easier

For many new SMBs, their lack of financial history makes it challenging to obtain financing. Traditional business credit scores tend to rely on many months of historical financial data that simply does not exist. The perceived risk of new SMBs can cause hesitation within credit unions and community banks to help – although we know it is in your DNA to do so. So how can an innovative SMB lending platform make a difference here?

It is all about the power of alternative data intake. This means working with more relevant and timely information, such as cashflow data from monthly bank statements, that enables SMBs to build up a credit history faster.

Alternative data is the key to understanding things such as different operations models, the seasonality of a business, or the true impact of the pandemic. The better you are at collecting, monitoring and deciphering the business nuances of every individual business, the more you can adapt your machine learning credit models to the economic fabric that makes up business segments within your community. This is the answer to lending more while controlling risk.

Providing the business insights and advice SMBs need to grow their business

Once you have unlocked alternative data sources such as cashflow, you can start to look at offering powerful business insights that help SMBs grow their business. This data can be continuously analyzed to proactively evaluate SMB financing needs – be it for expansion projects or for supporting economic recovery. Imagine equipping your small business lending team with the post-lending analytics they need to increase communications and offer advice that will help SMBs succeed. Sounds like higher profitability and more meaningful relationships for all involved.

In summary, to meet the needs of small business owners, you must be prepared to combine your “local people who really care” superpower with a bit of technology innovation. It has to be both, and the faster the better. You are facing fierce competition from the likes of big banks and fintechs – but localization and people power will give you a non-replicable advantage. If you can commit to paving a faster path to financing, making it easier to obtain credit, and providing valuable business insights that enable SMBs to grow their business, you will naturally win.

Stay tuned for the next few blogs, where we’ll dive deeper into other elements that can strengthen your business case for SMB lending innovation. Part 2 examines the annual SMB loan review process, and introduce the concept of an all-the-time review process. Part 3 discusses the benefits of a cloud-based approach to SMB lending.

Ready to learn more about our AI-driven SMB lending platform? Submit a demo request today and our team will be in touch shortly.

Share this article

Related Posts